Two-thirds of European Union member states are failing to provide the corporate tax incentives necessary to shift commercial fleets away from fossil-fuel vehicles, according to a new analysis by Transport & Environment (T&E). The study reveals that in 18 out of 27 EU nations, the fiscal gap between electric vehicles (EVs) and internal combustion engine (ICE) cars remains insufficient to offset the higher upfront purchase price of electric models.

T&E warns that weak company car tax structures risk locking the continent into a long-term reliance on oil imports from volatile petrostates.

To evaluate the efficacy of national tax regimes, the environmental campaign group assessed whether the corporate tax differential exceeded the average EV price premium, which stood at €10,650 in 2025. T&E reasoned that where tax structures fully neutralise this upfront capital premium, the lower operational and running costs of EVs establish a clear business case for corporate electrification. However, the study found that the tax gap surpasses this price premium in only nine EU countries.

Corporate vehicles represent a critical lever for reducing road transport emissions, accounting for 59 per cent of all new car registrations and 78 per cent of the petroleum consumed by newly registered vehicles across the bloc.

To address this, the European Commission introduced the Clean Corporate Vehicle regulation, which proposes national electrification targets for large corporate fleets, aiming for an EU-wide average of 45 per cent of new company vehicle registrations to be fully electric by 2030. Under the current proposal, member states—rather than individual businesses—would be held legally accountable for meeting these benchmarks.

T&E strongly backed this regulatory approach, noting that member states hold the fiscal tools necessary to widen the tax gap between different powertrains. In nations where such structural reforms have been enacted, corporate EV adoption has accelerated dramatically:

- Belgium: Following tax overhauls enacted in 2021, corporate EV registrations climbed from 8.8 per cent to 54.2 per cent in 2025.

- France: Sequential regulatory reforms implemented across 2024 and 2025 pushed the electric share of corporate car registrations to a record 41.3 per cent in March 2026.

Conversely, the EU’s other major automotive markets—Germany, Spain, Italy, and Poland—have yet to execute the fiscal reforms required to make the corporate tax gap exceed the EV price premium.

Stef Cornelis, Fleets and Freight Director at T&E, commented on the findings, stating: “At a time when the EU wants to cut oil dependency, governments of the EU’s largest car markets are failing to incentivise companies to go electric. The EU fleets regulation is the catalyst needed to break this inertia. The EU Council and EU Parliament should inject more ambition into the Commission’s proposal to ensure Europe can reduce oil imports rapidly.”

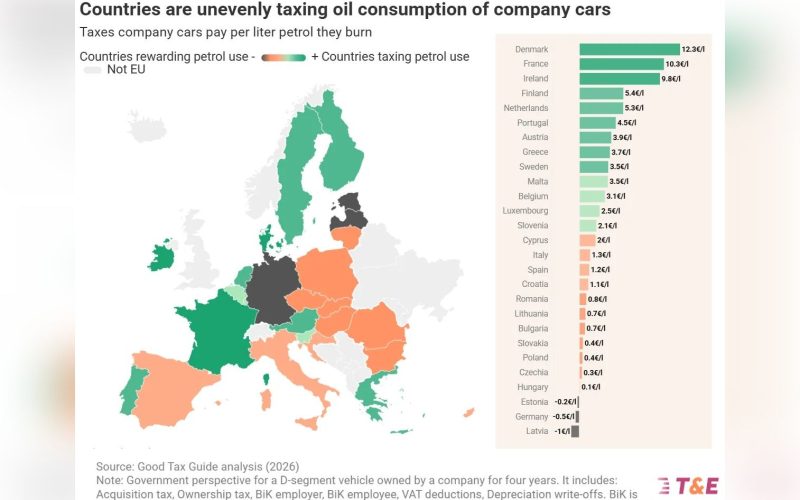

The report highlights that 13 member states continue to provide implicit or explicit financial subsidies to corporations operating petrol-powered vehicles. Germany emerges as a primary outlier, accounting for 28 per cent of all new fossil-fuel corporate car registrations in the EU. German companies receive a net €10,000 fiscal subsidy per vehicle—more than double the rate of any other member state.

In stark contrast, France levies €25,000 in taxes on corporate petrol registrations, while Denmark—which tops the European tax-gap rankings—charges €37,000.

These divergent tax frameworks create vast discrepancies in state revenue and environmental impact across the region. While Germany provides an effective subsidy equivalent to €0.50 for every litre of petrol burned by its corporate fleet, the French treasury generates a revenue equivalent to €10.30 per litre.

Similar imbalances persist on a regional level:

- South-West Europe: Portugal generates an oil revenue equivalent to €4.50 per litre, whereas Spain collects just €1.20 per litre.

- Eastern Europe: Slovenia leads the region by securing a revenue equivalent to €2.10 per litre, while Poland brings in only €0.40 per litre.

Together, Germany and Poland comprise 52 per cent of corporate registrations for high-consumption D-segment vehicles, yet both nations continue to apply weak tax penalties to these models. T&E notes that this lenient taxation drains corporate capital that could be reinvested elsewhere in business operations.

Furthermore, national tax frameworks are largely failing to progressively penalise the most polluting vehicle classes. While France doubles the tax burden for large E-segment vehicles compared to smaller C-segment cars, and Portugal increases it five-fold, most EU nations apply negligible tax escalations for larger body types. Germany again ranked as the least progressive system, providing an even larger effective subsidy for high-emission E-segment corporate cars than for smaller C-segment vehicles.

To rectify these market distortions, T&E is urging European lawmakers to preserve and enforce provisions within the Clean Corporate Vehicles regulation that would eliminate all subsidies for petrol cars, restricting financial incentives exclusively to electric vehicles manufactured within Europe.

Stef Cornelis added: “It’s perplexing that in almost half of EU countries, governments are still giving a subsidy for companies to drive a petrol car. Lawmakers and Member States must defend the provision that financial benefits can only be given to a company car when it is electric and produced in Europe. This way we create jobs locally, reduce oil imports and safeguard the future of Europe’s auto industry.”